Design Thinking Excercise

A Low Fidelity Wireframe based on User Research for a class project.

In this initiative, they have detected issues that traveling customers have had with their cards, and are looking for a digital solution to add as a feature to their application.

I created a research plan and some interview guides, before embarking on my first user experience interviews.

Purpose

The purpose of this research is to interview users in order to identify pain points, insights and their point of view when it comes to traveling with their cards overseas.

Method

Research will be conducted in person, via one on one interview, these sessions will last 30–45 minutes. The questions will be printed out beforehand and participants will not have access to them before the interview. Participants will be aware that this information will be used to create a feature on Whole Bank’s app.

Participants

Participants will range from 21–65 years of age, must be have traveled in the past year and have a debit or credit card. Participants will be recruited through my personal network of friends and family.

Location

Interviews will be conducted in the participants residence.

Most of the questions are open ended, or probing questions to see if we can uncover more information. However; in every single interview, when they provided opportunities to elaborate more on their point of view, it was better to follow that thread that stick to the script.

There were 5 participants and 4 pages of notes for each, this part was what took the longest to do. Next time, I will not make the same mistake of scheduling two interviews back to back, its a bad idea.

Henry, Doctor, Age 52

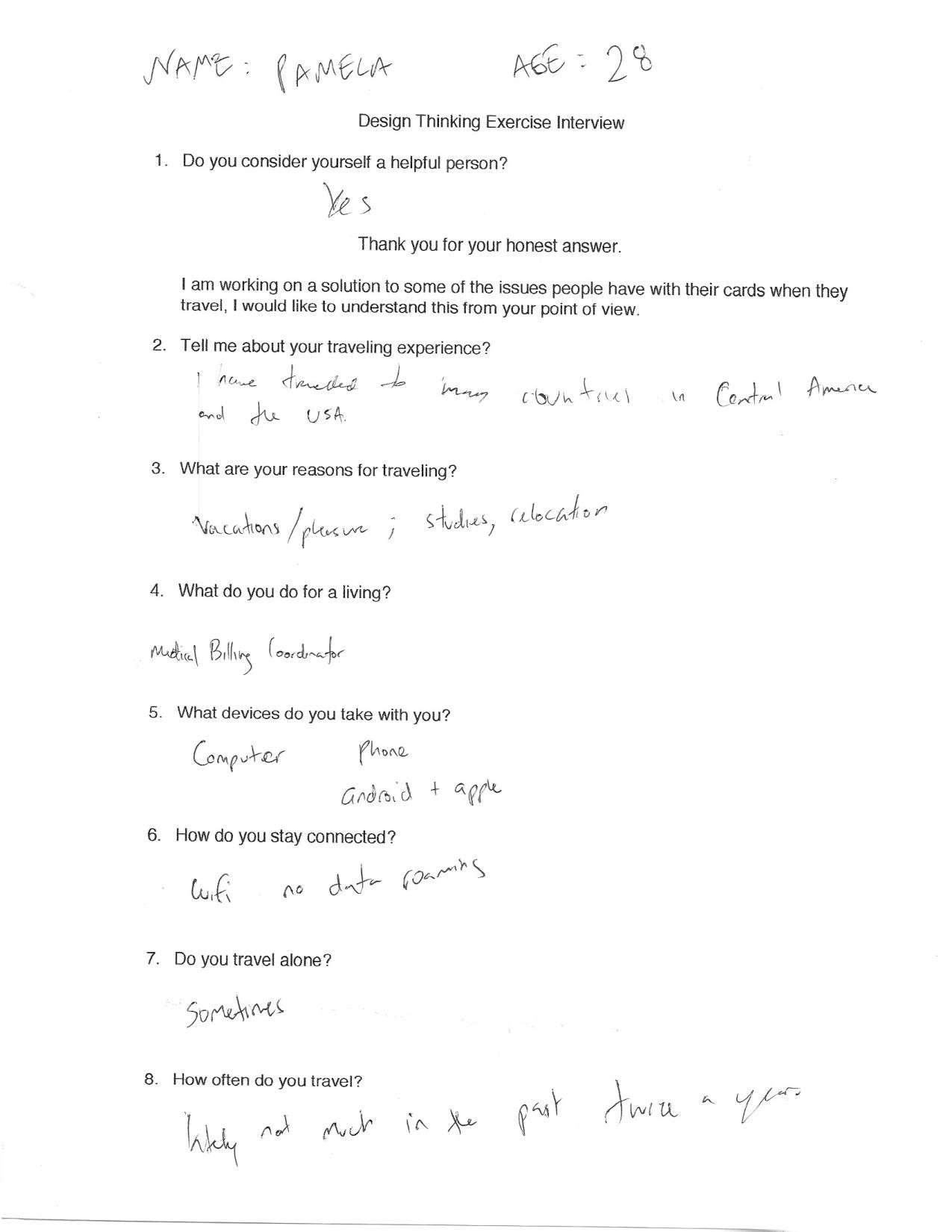

Pamela, Billing Coordinator, Age 28

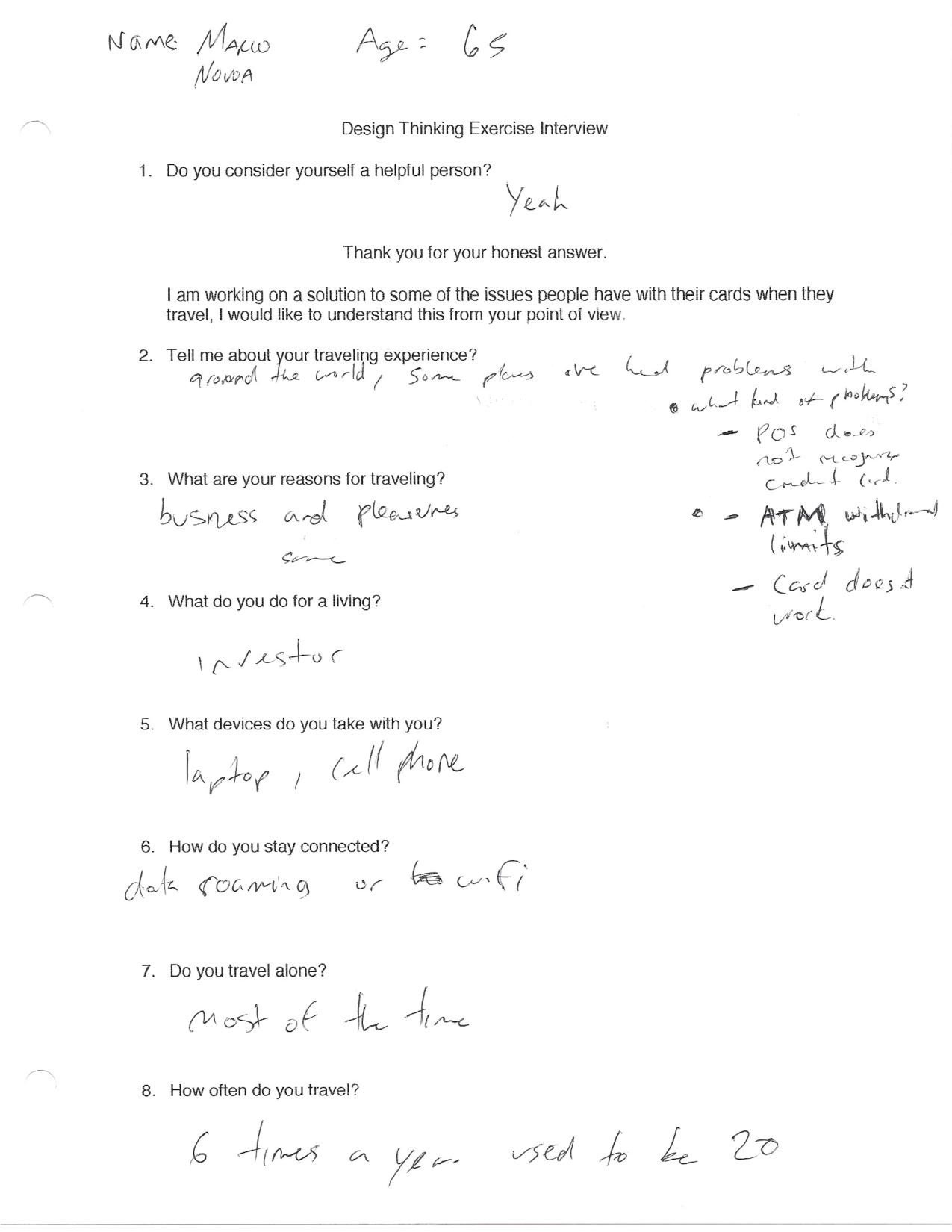

Marco, retired, Age 65

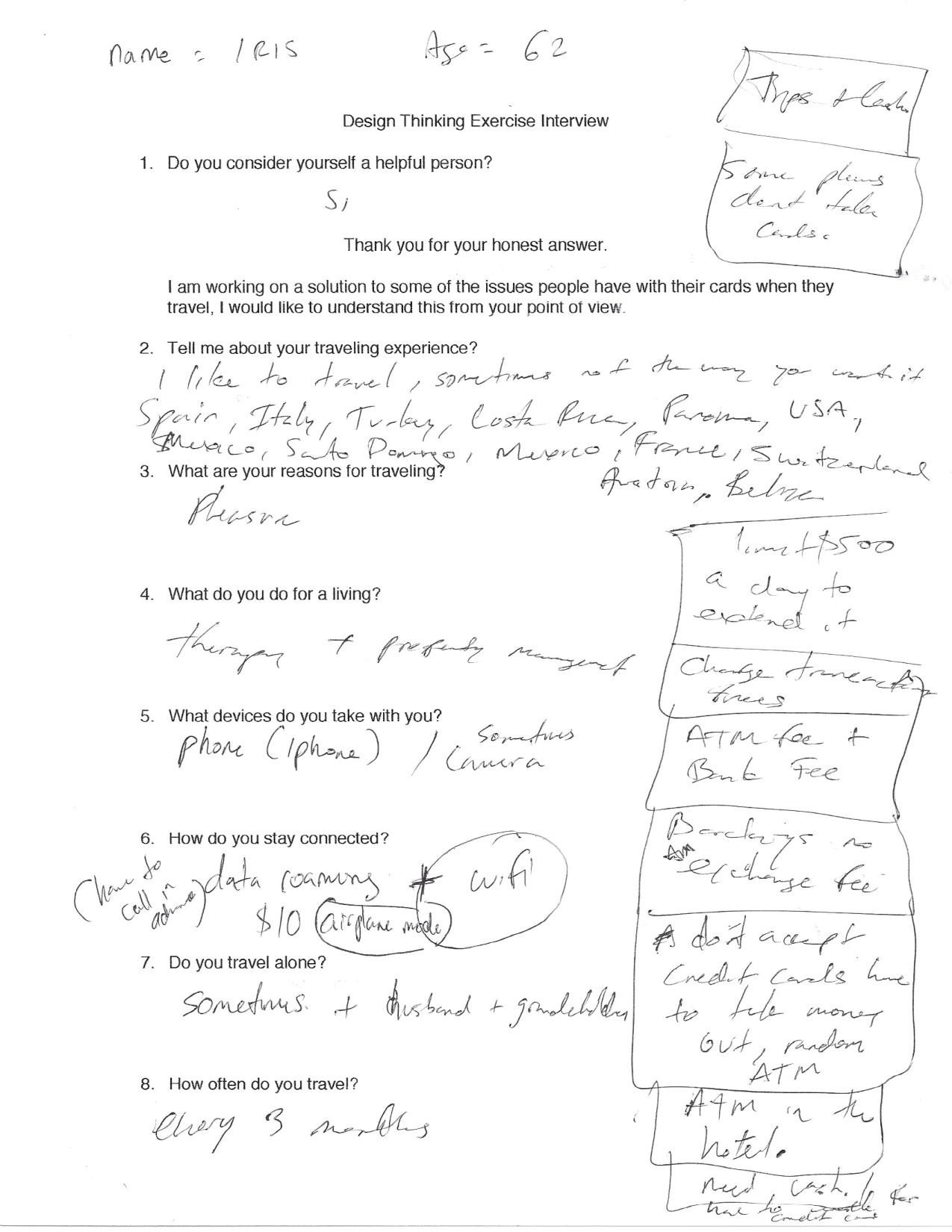

Iris, Property Management, Age 62

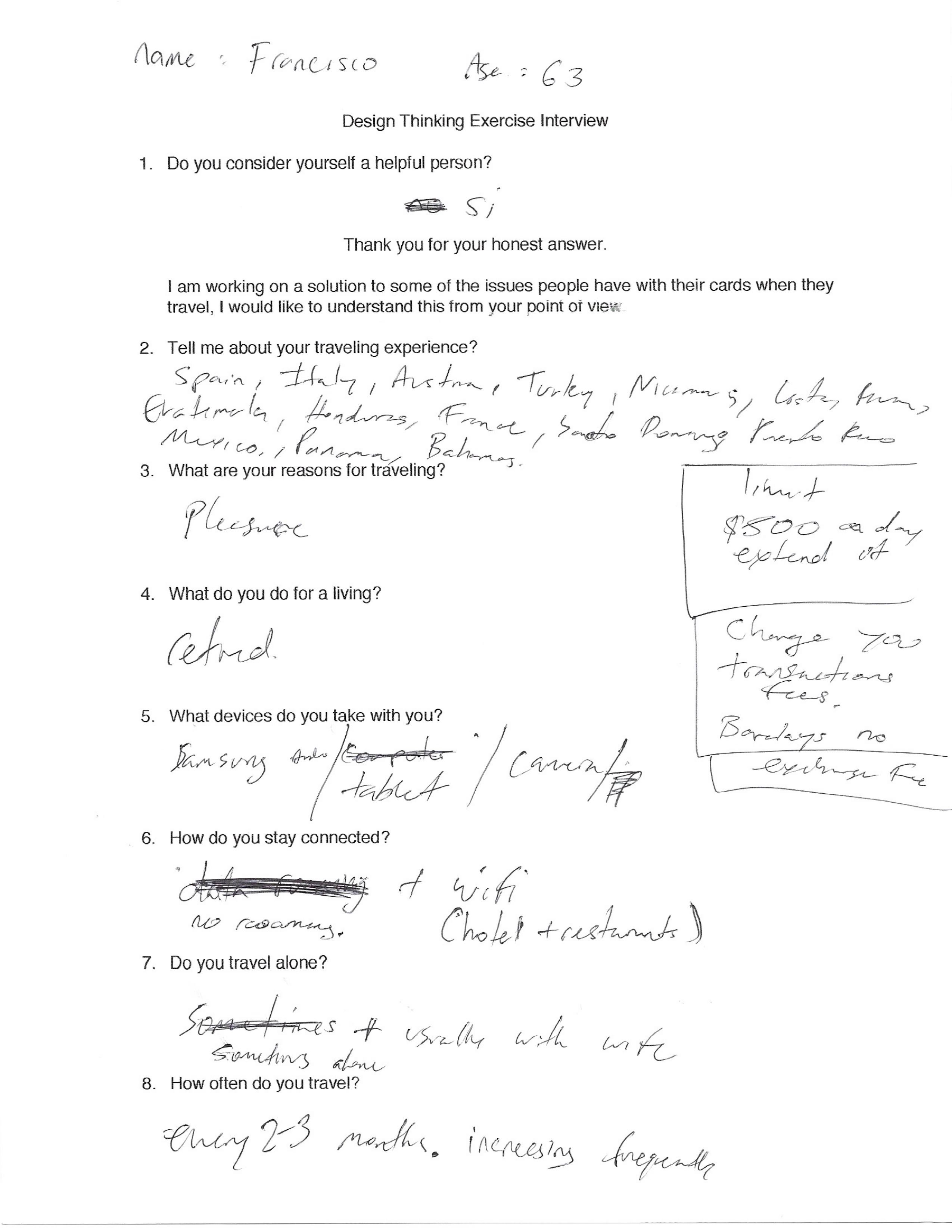

Francisco, retired, Age 63

In the next stages, it was helpful to think along the following lines:

Would Iris use this?

Is this easy enough for no-nonsense Francisco?

The design was made with them in mind. I have included two of the persona profiles to focus on the other stages.

Francisco is 63 years old, married, retired. He travels every 2–3 months for pleasure. Usually with his wife Iris. Once a year he travels with his grandkids, and his kids and brother-in-law. He travels with an Android phone and an iPad, but only connects to Wifi.

He was pickpocketed in Spain 10 years ago, but was able to get the money back because he caught one of the thieves. He is concerned with security and who he gives his personal information to when traveling.

Iris is 62 years old, married, she works in property management. She travels every 2–3 months for pleasure. Usually with her husband Francisco. Once a year she travels with her grandkids, kids and brother. She travels with an iPhone, she has had to pay more than $300 dollars in data roaming charges in the past so she is careful to have her phone in airplane mode, with wifi activated. In a pinch she would activate roaming but she says it costs her $10 per day.

She loves to travel and is currently exploring Europe every 3 months. When she travels she is concerned with transaction fees, exchange fees, and ATM charges that she says can take hundreds of dollars from a trip.

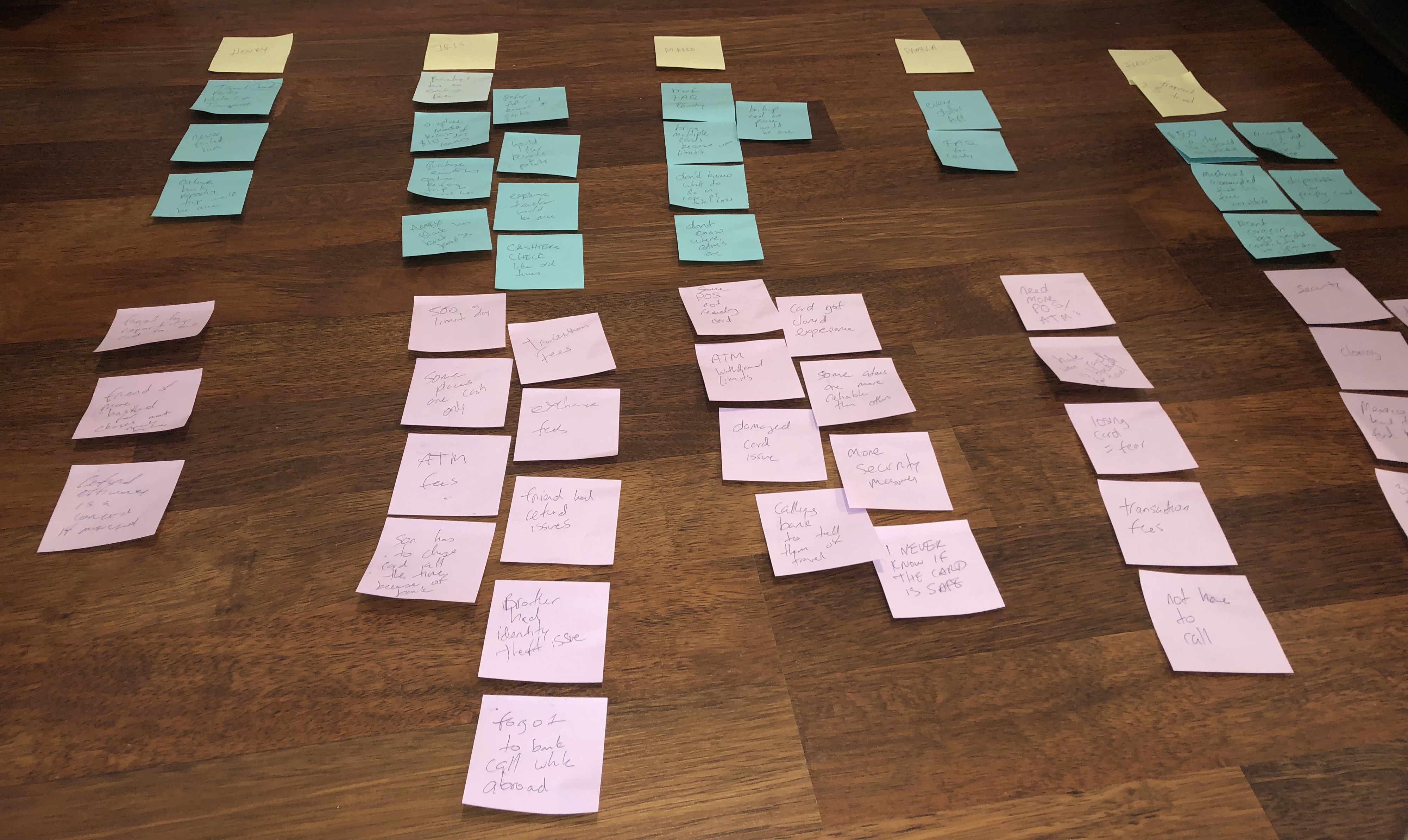

This is the stage where I began to define the problems and the needs of the user, without losing track of the business needs.

Round 1

Yellow — Users (Henry, Iris, Marco, Pamela, Francisco)

Green — Insights

Red — Pain Points

Organized each interview, in a way where red are complaints, and green are suggestions or wants they mentioned.

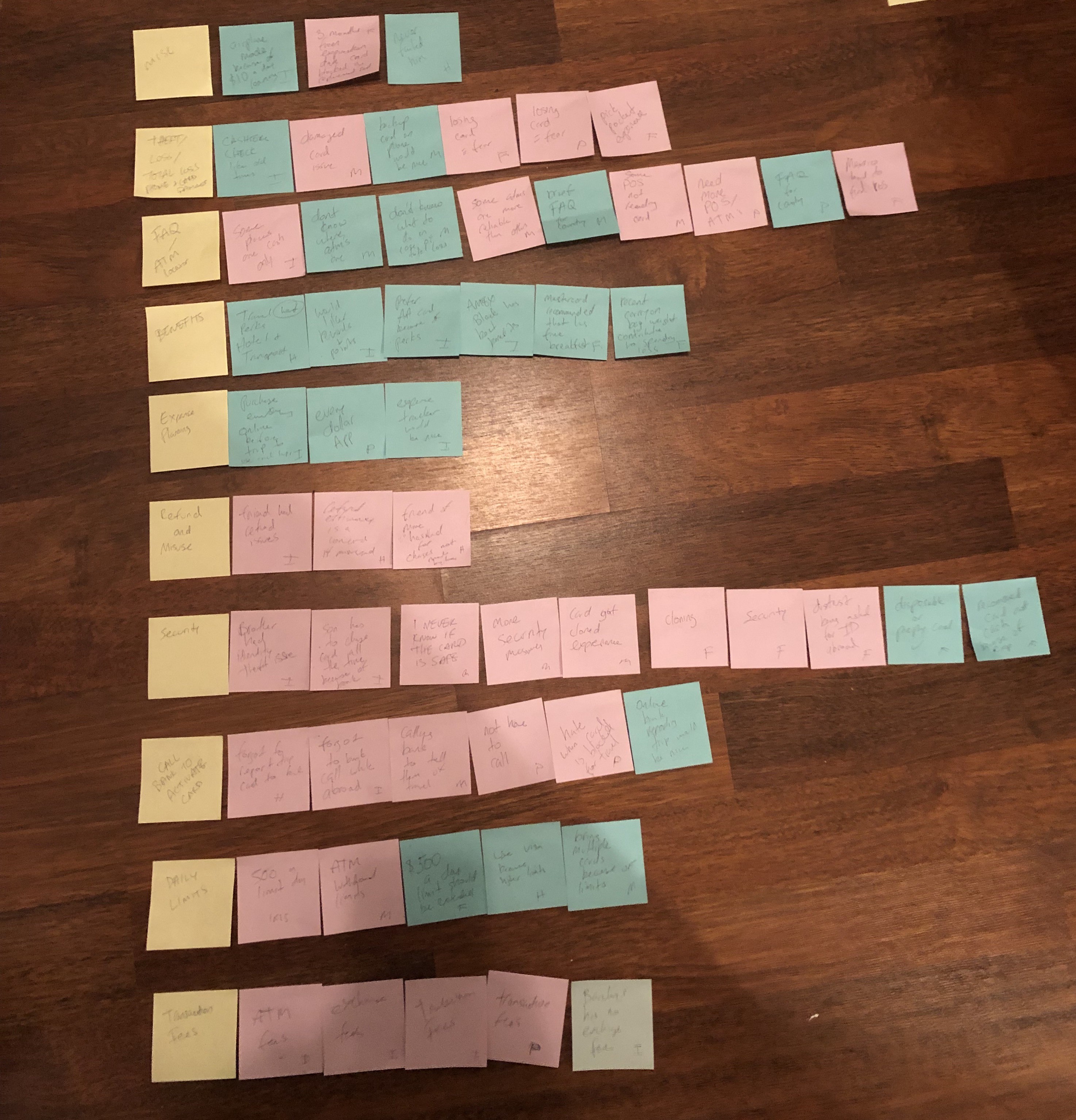

Round 2

Yellow — Themes that could be linked to the interviews appeared, and reorganized post-its to each of these.

Problems found as a result of the research and defining stages are the following:

Transaction Fees — Some cards have lower transaction fees than others, typically ATM’s also have fees for travelers, there are also disproportional exchange rate fees.

Daily Card Limits — $500 daily maximum seems to be a common issue, sometimes when checking out of a hotel, the transaction can easily go past that limit and cause embarrassing issues in the lobby, when the card is declined, despite being in good standing.

Having to Call the Bank before leaving — This is the number one issue that was commonly reported. The hassle of having to wait in queue over the phone with customer service to report that they are traveling.

Security Issues — Card cloning happened to one of the users, and there is a general fear of the card having charges added that they did not make, for one they realize sometimes in the monthly statement the error.

Refunds and Misuse — The refunding and claim process is perceived as being stressful. It also takes a long time.

Expense Planning — the ability to plan their expenses and see how much they are spending is appreciated by the users. They mention Chase offers a service where text messages are sent when transactions exceed $50 and they like to know that type of information.

Cardholder Benefits — this is another big category, although not a problem but more of a desire. There is a reverence for the Black American Express card and the benefits, refund policy and miles program. The American Airlines is another card that is liked because of the miles program.

Country- Specific FAQ and ATM locations — specifically to banking when traveling, and things like etiquette, manners and respect in different cultures would be nice to have.

Loss (Theft, Phone and Card ) — loss is a big fear, specially because of the perceived consequences of what could be done with their card and information. all users found it hard to imagine a scenario where they had no phone and no card. There would have to be an option online where they could be issued something similar to a travelers check.

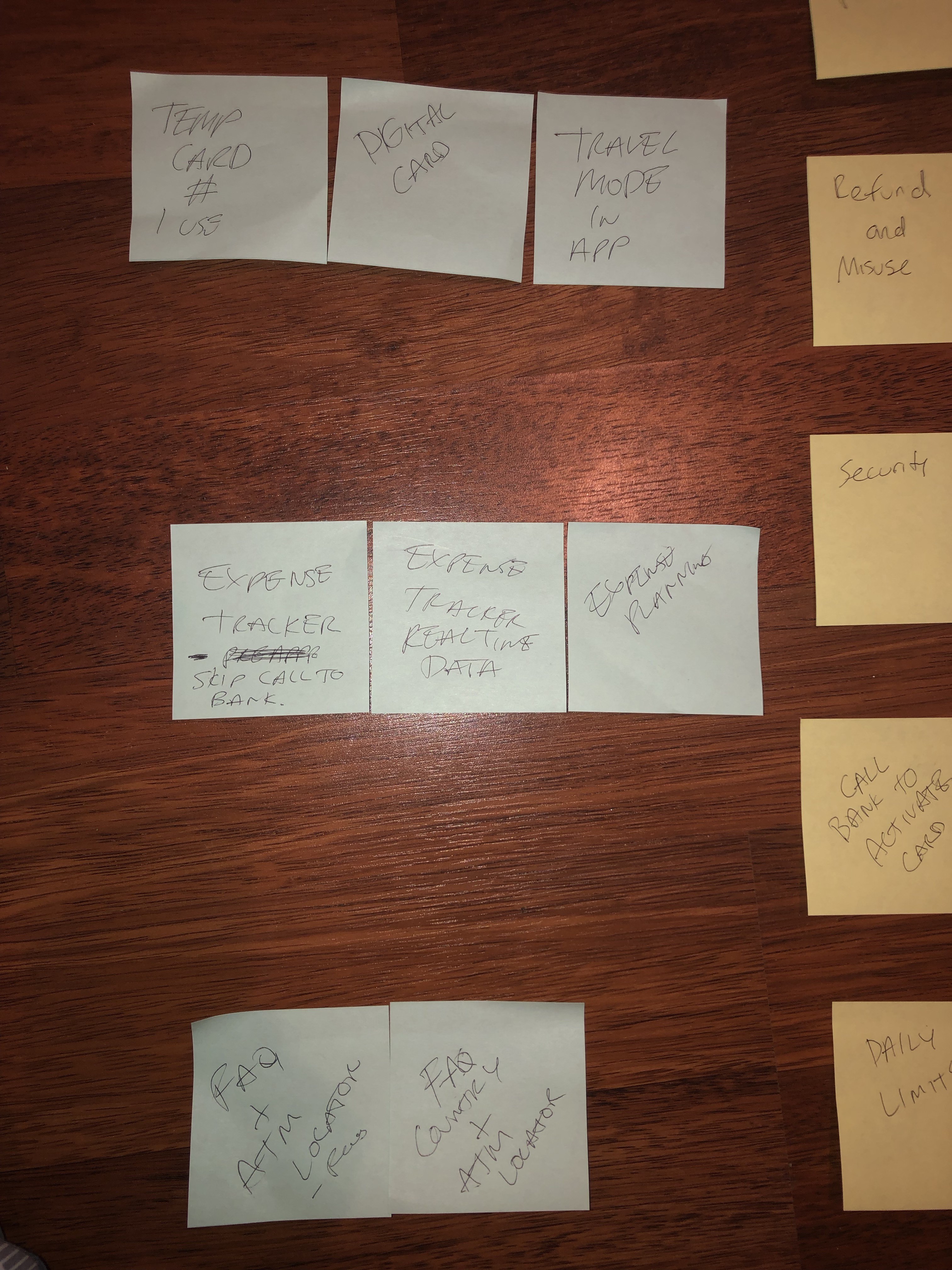

Once the problems are defined, and grouped into themes . The next step was to come up with possible solutions for each problem.

Round 3

A trick to solve problems is to create a representation of the answer. So that the answer already exists. This was inspired by an entrepreneur who shared the concept with me of Forward Directed Therapy (FDT) from the book Think Forward to Thrive .

In a way it functions as a placeholder, that the problem has a solution.

Round 4

Next to each themed problem defined in the last stage , Iplaced a solution for that specific problem.

Once I was done, I grouped these together.

So the Features required to solve the most amount of issues the users mentioned came down to the following:

FAQ section for country specific questions + ATM locator

Expense Tracker with realtime tracking and a way to skip calling the bank

Travel Mode for the app with a digital payment system and a temporary card number per transaction in case of RFID theft or cloning.

During the process I was already curious about what technologies where available. I knew RFID existed but has its limitations that Point of Sale(POS) devices have to have that. What surprised me was learning about the $25 million dollar acquisition Samsung made of a company called LoopPay that patented Magnetic Secure Transmission (MST), basically your phone can function like a regular card in any POS (That makes it easier to use the phone like a card anywhere a card is accepted). Currently LG has developed a similar technology that is able to do the same. The options later on in development could be A) develop in-house the MST technology (expensive) B) buy or make a deal with a developer who already has that technology (expensive) C) piggyback on the technology, Android users can activate their card on SamsungPay and use that technology, Apple users would only be able to use RFID (practical solution). The assignment is specific that everything must be done in app so while RFID is a given, the capabilities of MST depend on how much Whole Bank wants to invest.

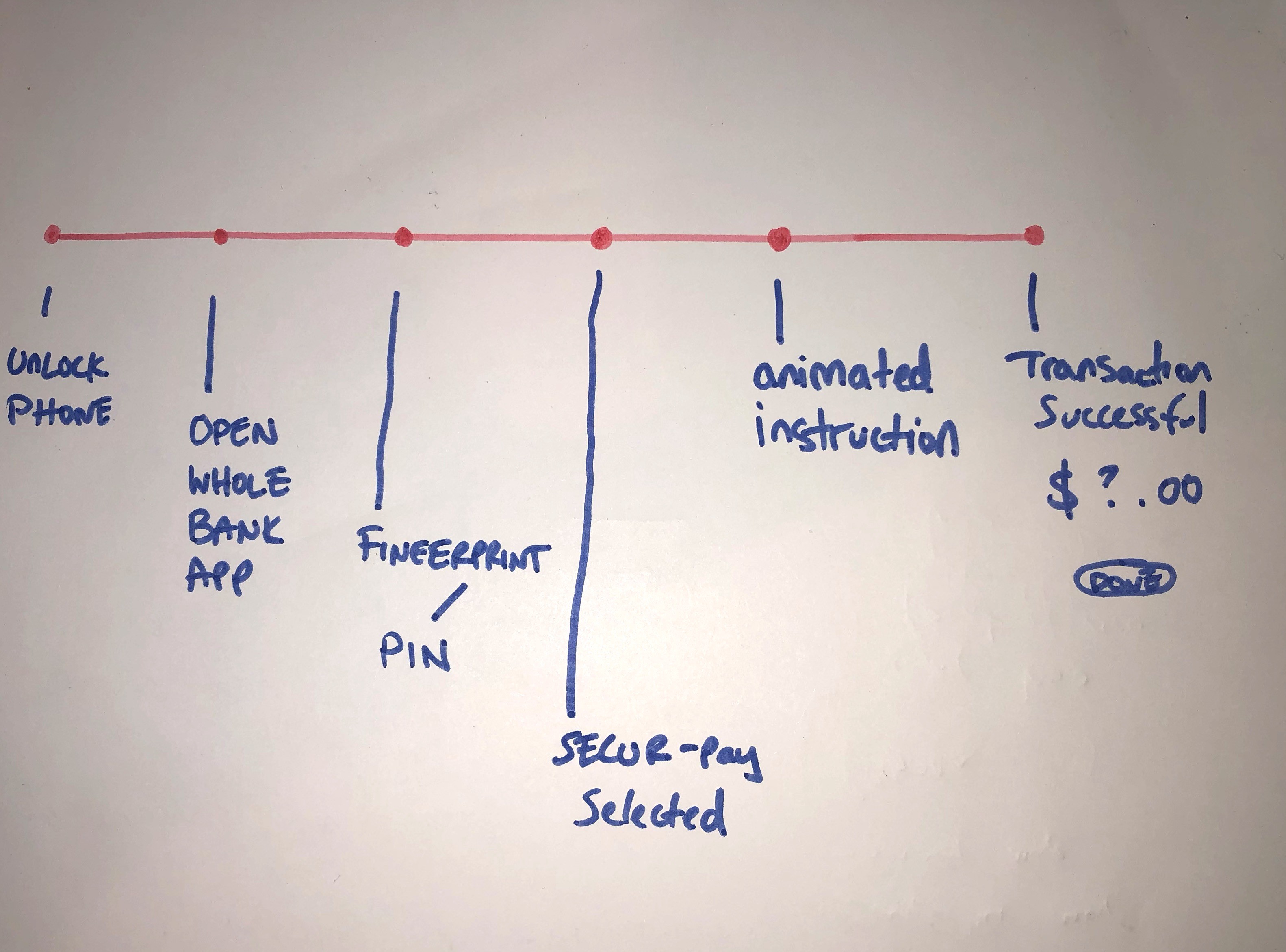

Imagine you are in a coffee shop and need to make a payment. 1st you unlock the phone then you open the app.. you get the idea. The relief one has once the app is ready to go, those minor pet peeves also count towards the overall feeling of the app. There should be a minimum amount of effort to get the payment section to start working.

Based on some of the concerns the users had, the names for the features or screens where chosen so that an association with certain words can be perceived.

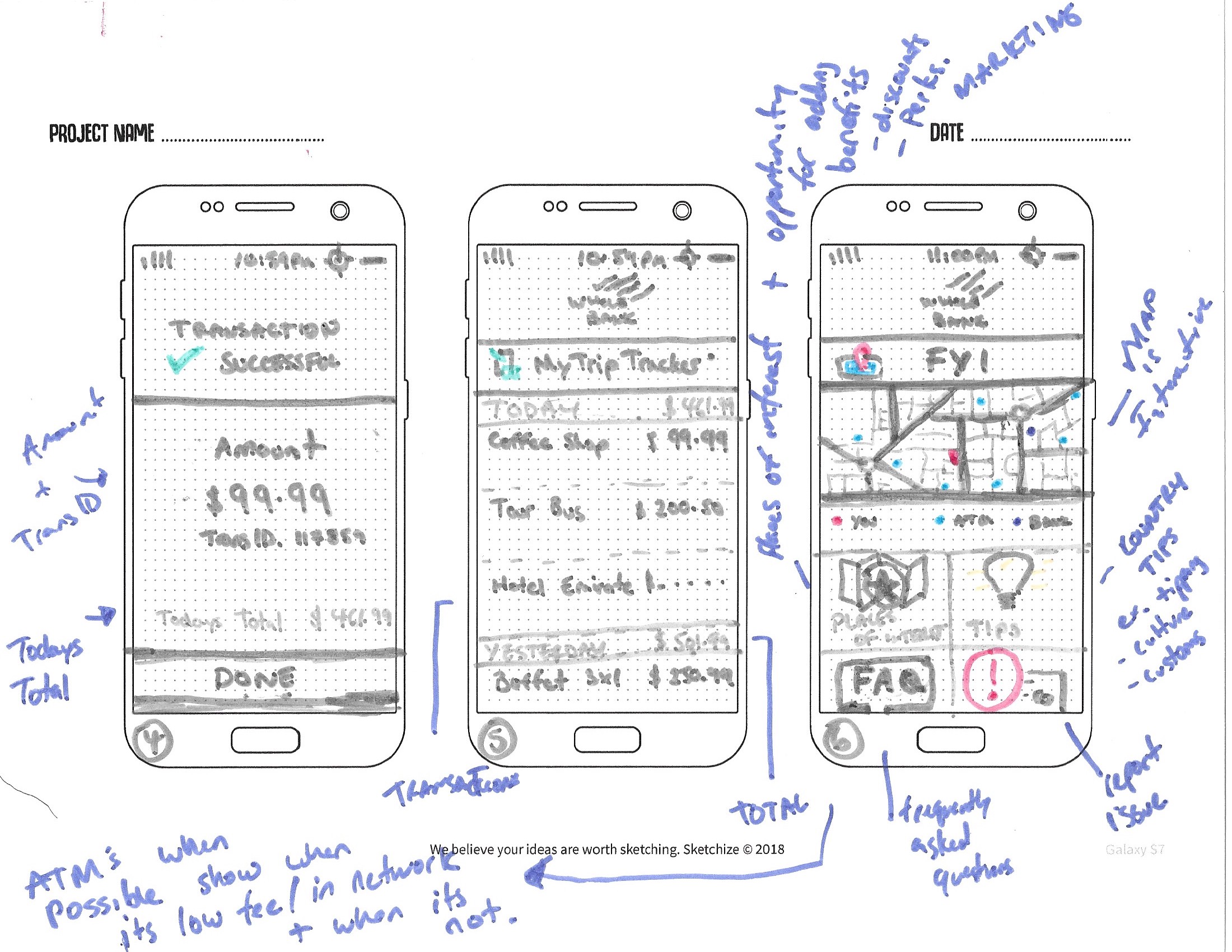

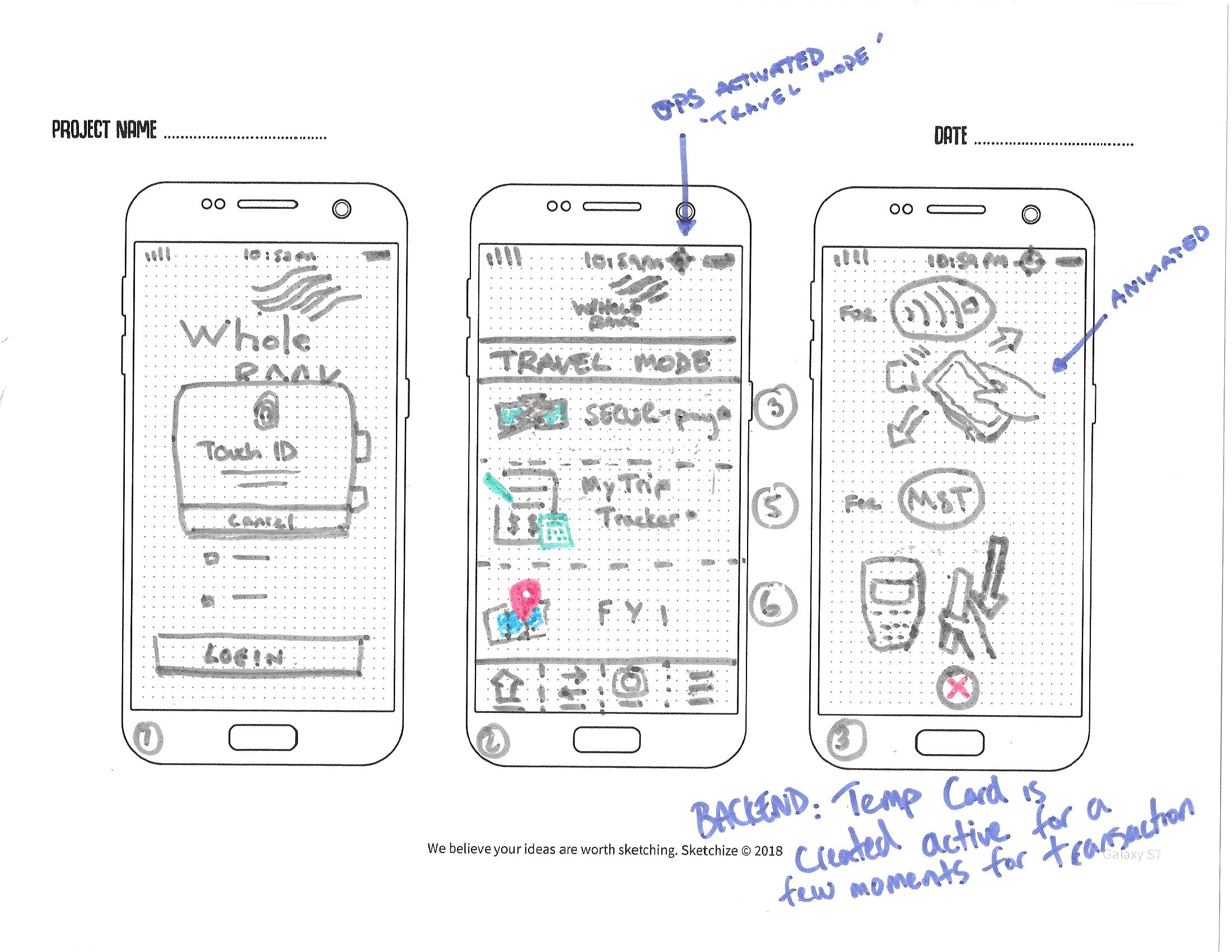

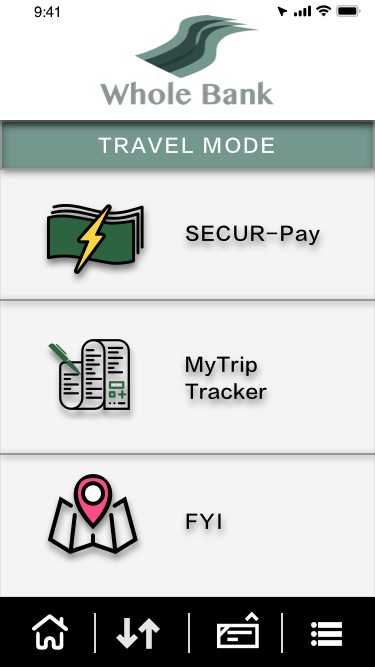

The feature in the Whole Bank app is called Travel Mode.

The payment part of the app is called SECUR-pay (security).

MyTrip Tracker is the part of the app to track use and payments.

FYI (For Your Information) with a map icon, represents the FAQ and ATM map as well as other stuff.

While doing the wireframe, a better idea popped up. GPS location on the phone automatically activates Travel Mode and the log that the user is in Travel Mode, creates an update in the bank database; this eliminates the need for the user to call or even press a button to inform the bank that they are outside the country.

Screen #1 is a simple login, that prompts for fingerprint for faster authentication

Screen #2 is the Travel Mode main menu, yet still retains some of the functionality that a normal bank app would have in the bottom navigation bar.

Screen #3 has animated pictures, to simplify how to use the SECUR-pay feature.

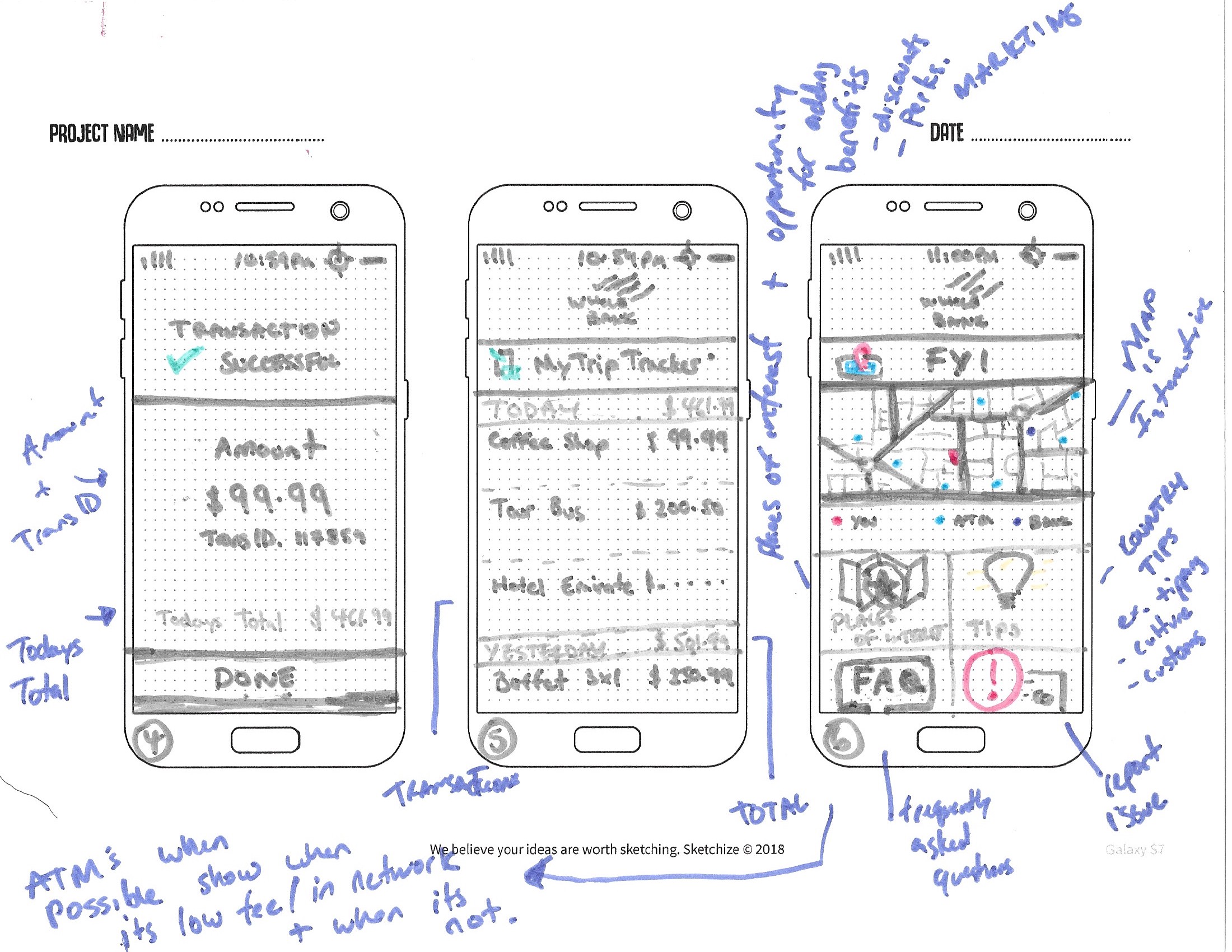

Screen #4 Tells the user that the transaction went through, they can double check the amount, and see an updated total for the day.

Screen #5 MyTrip Tracker is a log of the transactions made, from most recent to last.

Screen #6 Has a map that expands when selected. Shows ATM’s and Banks where WholeBank can negotiate the best possible way to reduce the transaction fees the users reported disliking.

Also has FAQ for the app and features.

Tips tailored to the geolocation — things such as tipping, culture, references, contact numbers, etc

The places of interest button can be an opportunity to create deals, discounts and other benefits for customers while they travel, like GoogleMaps but curated by Whole Bank.

How does the prototype measure up to the problems identified in the research.

Transaction Fees — The FYI feature has a map that can locate ATM’s and can label ones that are more favorable to use for the user

Daily Card Limits — Instead of calling to authorize a transaction that goes over that amount, using the app and being aware of one’s spending with MyTrip Tracker and the prompts when paying as well as the fact that it requires fingerprint authorization can eliminate the liability the bank would have if the customer goes over.

Having to Call the Bank before leaving — Using geolocation and activating Travel Mode, tells the bank that you are traveling. No need to call anymore!

Security Issues — card number created/used for the transaction only exists during the duration of the transaction. If it is intercepted it will only function for a few seconds to minutes.

Refunds and Misuse — MyTrip Tracker, can help identify issues before the monthly statement reaches you, and allows for prompt reporting of an issue. As well as a more informed user about their finances.

Expense Planning — MyTrip Tracker tells you how much you spent per day, so that users can keep track. Future iterations can include budgeting function.

Cardholder Benefits — The FYI feature includes a section for point of interest, this is where benefits, discounts and promotions can be placed.

Country- Specific FAQ and ATM locations — geo-location allows to show the user, an FAQ that is ‘country specific’, can include content about etiquette, customs, doing business, tipping guides. As well as a map to the closest ATM’s and/or banks.

Loss (Theft, Phone and Card ) — If the physical card is lost, or damaged this can be a work around, the use of MST technology makes any POS compatible with the phone, so theres no need for special equipment from the merchants. And can potentially be used with ATM’s.

What about total loss? In the case that the phone, and card are lost, a web-based feature to aid in the purchase of at least a phone to install the app on could be added in future iterations.

I will follow up with her to see what she thinks. Additionally, Henry, Marco, Francisco and Pamela. I guess this post is an iterative deal as well.

In the beginning of the project some keywords where put in bold to check if this project meets the vision Whole Bank tasked us.

Whole Bank started its operations in Framingham, Massachusetts. Their goal was to offer a different way to save and manage money by giving customers innovative options such as virtual currencies.”

The bank is in a transitioning period, moving from a traditional bank to a more technological and user-friendly company.

In this initiative, they have detected issues that traveling customers have had with their cards, and are looking for a digital solution to add as a feature to their application.

Based on this information about the client, we can ask these questions about the design:

It was necessary to treat this as if it was real world scenario. There are probably a lot of things that can be done easier than I did them. A lot of the research and studying to learn the process is making sense. One interesting thing that worked is to acknowledge that I wanted this project to go one direction from the get-go, and that not recognizing ones own point of view could affect interviews and data gathering. It is necessary to separate one’s point of view from the users, to appreciate their way of seeing the world. Had I gone with what I thought this would have been a failure.

Most important lesson learned, is that design thinking works better than other methods when you go with the flow of what the users are telling you. They will point you in the right direction.